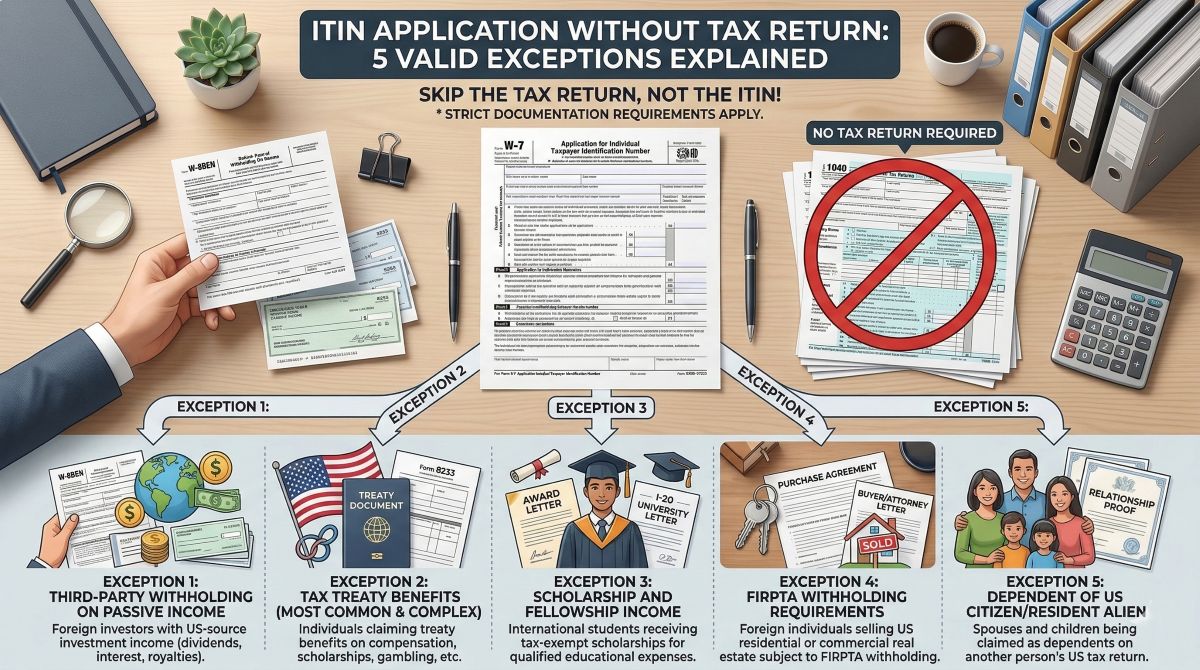

Yes, you can apply for an ITIN without filing a US tax return if you qualify for one of five IRS-approved exceptions. These exceptions allow specific individuals—such as foreign investors receiving passive income, international students on scholarships, treaty benefit claimants, real estate sellers, and qualifying dependents—to obtain an Individual Taxpayer Identification Number without submitting a federal tax return alongside Form W-7. Each exception category has strict documentation requirements and specific eligibility criteria that must be proven to the IRS.

Disclaimer: This guide provides general information about ITIN exception categories based on IRS Form W-7 instructions. Tax situations vary significantly based on individual circumstances. For personalized guidance on which exception applies to your specific situation, consult a tax professional or Certifying Acceptance Agent.

| Field | Information |

|---|---|

| Can you get an ITIN without a tax return | Yes, if you qualify for an exception |

| Number of exceptions | 5 main exception categories |

| Most common exception | Exception 2 (Tax treaty benefits) |

| Required with the application | Supporting documentation proving exception eligibility |

| Processing time | Same as regular applications (7–11 weeks) |

| Still need Form W-7 | Yes, except for the reason code selected |

Most ITIN applicants must attach a federal tax return when submitting their Form W-7 application to the Internal Revenue Service. However, five specific situations exist where the IRS allows individuals to apply for an ITIN without including a tax return.

These are formal IRS-recognized exceptions documented directly on Form W-7, each requiring comprehensive supporting evidence and proper documentation to prove eligibility. You cannot simply skip the tax return requirement without meeting specific exception criteria established by the IRS in their official guidelines.

Using an exception means you do not attach a tax return to your Form W-7 application when submitting to the IRS. However, the exception does not mean you do not need an ITIN or that you are exempt from all tax obligations.

The Internal Revenue Service recognizes exactly five exception categories that permit ITIN applications without attached federal tax returns under specific circumstances.

Exception 1 covers third-party withholding on passive income received by foreign investors from US sources requiring identification number reporting.

Exception 2 addresses tax treaty benefits and includes four distinct subcategories covering compensation, scholarships, gambling winnings, and other treaty-covered income types.

Exception 3 applies to scholarship and fellowship income that is exempt under US tax law rather than international treaty provisions.

Exception 4 covers Foreign Investment in Real Property Tax Act withholding requirements when foreign individuals sell US real estate.

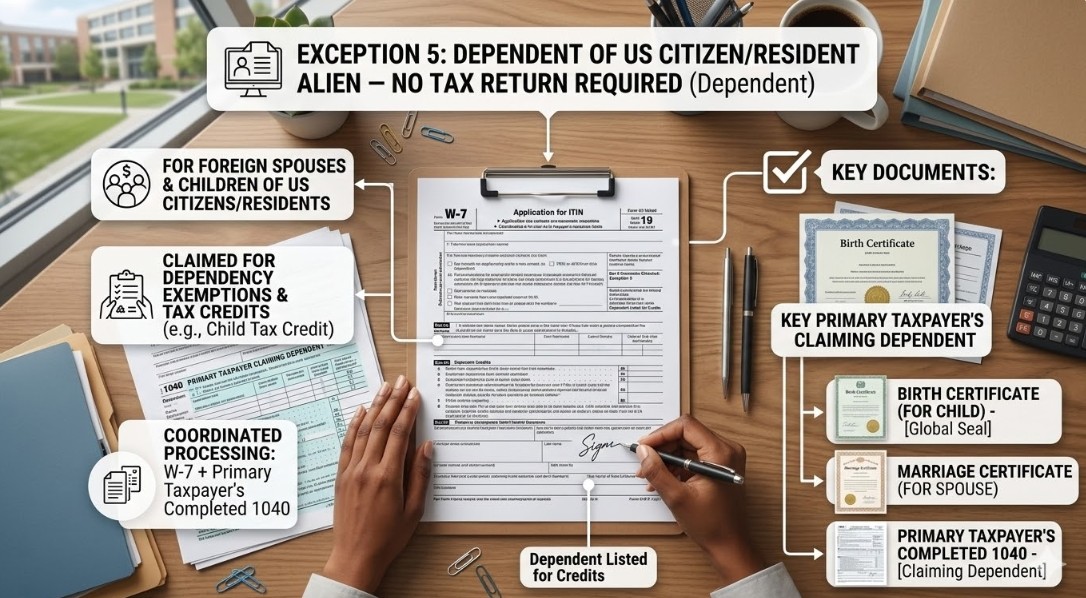

Exception 5 addresses dependents of US citizens or resident aliens who are being claimed on someone's tax return but have no independent filing requirement.

On Form W-7, Line 6h asks applicants to identify the reason they are submitting the form. Exception applicants must check the applicable box corresponding to their specific exception category and provide all required supporting documentation.

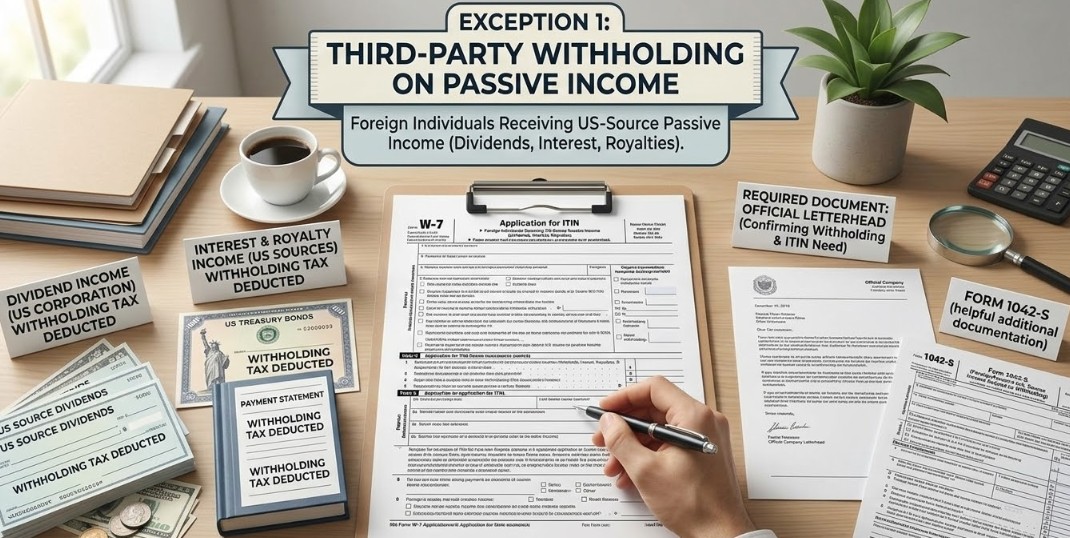

Exception 1 applies to foreign individuals who receive US-source passive income subject to tax withholding by a US payer or withholding agent. This exception typically benefits foreign investors who are not actively engaged in US business operations but receive investment income from US sources.

The income must be passive in nature—such as dividends, interest, or royalties—rather than compensation for services or active business income. The key distinguishing factor is that a third party withholds tax at the source before the foreign individual receives payment.

Foreign investors receiving dividend payments from US corporations through brokerage accounts where the broker withholds tax qualify for this exception. Foreign authors, artists, or inventors receiving royalty payments from US publishers, galleries, or licensees where the payer withholds required percentages also qualify.

A letter from the withholding agent on official company letterhead is the primary required document for Exception 1 applications. This letter must explicitly state that they are withholding tax from your income and confirm that your ITIN is required for reporting.

Form 1042-S showing the actual withholding that occurred is helpful additional documentation if available from the withholding agent. Active business income from trade or business activities does not qualify for Exception 1 even if withholding occurs.

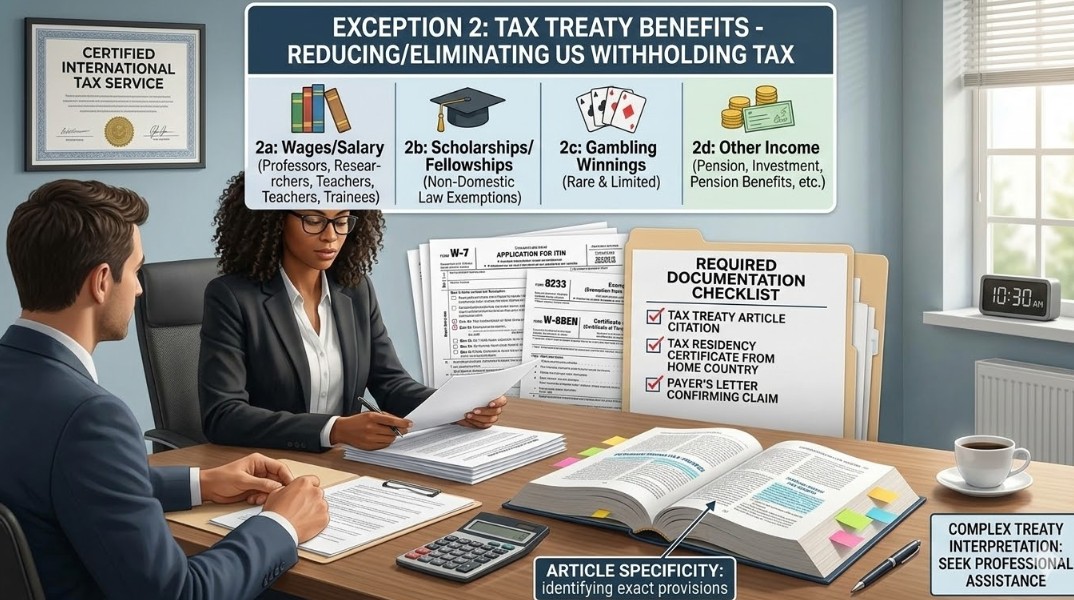

Exception 2 applies to individuals claiming benefits under international tax treaties between the United States and their country of tax residence. These treaties often reduce or eliminate withholding on specific income types, and individuals claiming these benefits may need ITINs for reporting.

This is the most common exception category and also the most complex due to varying treaty provisions between different countries. Exception 2 contains four distinct subcategories labeled 2a through 2d, each covering different types of treaty-benefited income.

Exception 2a covers wages and salary income exempt from US taxation under specific treaty provisions. This commonly applies to foreign professors, researchers, teachers, and trainees working temporarily in the United States.

Exception 2b addresses scholarship and fellowship income exempt under tax treaty provisions rather than US tax law. This differs from Exception 3, which covers scholarships exempt under the US domestic tax code without requiring treaty benefits.

Exception 2c covers gambling winnings exempt from US taxation under limited treaty provisions. This is rare because very few international tax treaties provide specific exemptions for gambling winnings.

Exception 2d serves as the catch-all subcategory for other treaty-benefited income that does not fit into subcategories 2a, 2b, or 2c. Examples include pension income exempt under treaty provisions or certain investment income covered by specific treaty articles.

All Exception 2 subcategories require Form 8233 (Exemption from Withholding) or Form W-8BEN (Certificate of Foreign Status) with the treaty claim documented. A letter from the withholding agent or payer confirming the treaty claim and stating that your ITIN is required.

Proof of tax residency in the treaty country through tax residency certificates issued by your home country's tax authority is essential. Treaty article citations must be specific and accurate, identifying the exact provision that exempts your income.

Complex treaty interpretation often necessitates professional assistance from experts in international tax services to determine whether income genuinely qualifies under Exception 2.

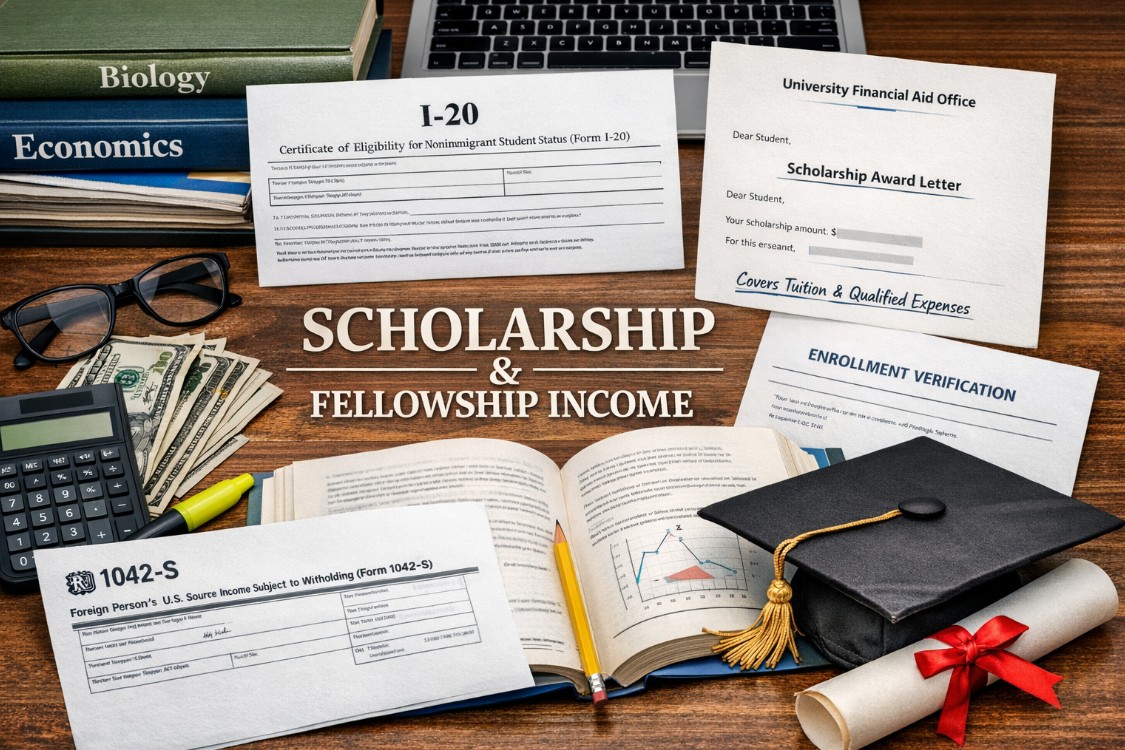

Exception 3 applies to international students receiving scholarship or fellowship income not subject to US tax filing requirements under the domestic tax code. This exception differs from Exception 2b because it is based on US tax law exemptions for qualified scholarships.

Students from any country can potentially use Exception 3 regardless of whether a tax treaty exists. The scholarship must meet IRS definitions of qualified educational expenses, including tuition, required fees, books, supplies, and equipment required for courses.

International undergraduate students receiving scholarships covering qualified educational expenses from US colleges and universities often qualify. Graduate students receiving fellowship grants for dissertation research or study, where the grant is not compensation for service,s also qualify.

The scholarship or fellowship award letter from the educational institution detailing the amount, purpose, and academic year is essential documentation. A letter from the university's financial aid office confirming that the scholarship covers qualified educational expenses only is also required.

Proof of enrollment, such as your I-20 form for F-1 students oran enrollment verification letter, is necessary. Teaching assistantships where students receive tuition waivers in exchange for teaching constitute wages and do not qualify.

Exception 4 applies under the Foreign Investment in Real Property Tax Act, which requires withholding when foreign persons sell US real estate. The buyer must withhold fifteen percent of the gross sales price and remit it to the IRS within twenty days.

The foreign seller needs an ITIN for proper completion of Form 8288 and Form 8288-A filed by the buyer or closing agent. This exception allows foreign real estate sellers to obtain ITINs without filing tax returns initially.

Foreign individuals selling US residential or commercial real property subject to FIRPTA withholding requirements qualify for this exception. Foreign heirs who inherited US real estate and are now selling the property can also use Exception 4.

A letter from the property buyer, buyer's attorney, or closing agent stating that FIRPTA withholding will apply is essential documentation. The letter must include the property address, anticipated or actual closing date, and an explicit statement that the seller's ITIN is required.

The purchase agreement or sales contract, demonstrating the transaction details, provides additional supporting documentation. Exception 4 applications are the most time-sensitive because real estate closings operate on strict timelines.

Exception 5 allows dependents who are being claimed on another person's US tax return to obtain ITINs without filing their own returns. The dependent has no separate US income or filing requirement, but needs an ITIN because the taxpayer claiming them requires identification numbers.

This exception is commonly used for foreign spouses and children of US citizens or residents when dependency exemptions or tax credits are being claimed. Foreign spouses being claimed on married filing jointly returns or foreign children being claimed for the Child Tax Credit qualify.

The taxpayer claiming the dependent must actually file a complete federal tax return, including the dependent on appropriate lines. The dependent's ITIN application is typically submitted together with this tax return to ensure coordinated processing.

The complete US tax return of the person claiming you as a dependent is required documentation. Birth certificates for children or marriage certificates for spouses demonstrating the relationship to the US taxpayer are also necessary.

| Exception | Who It's For | Required Documentation | Complexity |

|---|---|---|---|

| Exception 1 | Foreign investors with passive income | Withholding agent letter; Form 1042-S | Medium |

| Exception 2 | Treaty benefit claimants | Form 8233/W-8BEN; treaty docs | High |

| Exception 3 | Students with tax-exempt scholarships | Award letter; institution letter | Low-Medium |

| Exception 4 | Foreign real estate sellers | Buyer/attorney letter; purchase agreement | Medium |

| Exception 5 | Dependents on US tax returns | Tax return; relationship proof | Low |

Exception 3 (Scholarship) and Exception 5 (Dependent) are generally the easiest exception categories to document without complex legal analysis. Exception 2 subcategories represent the most complex applications due to tax treaty interpretation requirements.

Review the exception categories above to identify which potentially applies to your specific situation and income sources. Ensure you genuinely qualify before proceeding with application preparation, as misrepresenting your exception eligibility results in denial.

Collect all required supporting documents specific to your exception category using the documentation requirements outlined for each exception. Request necessary letters from withholding agents, educational institutions, employers, or other required parties well in advance.

Download the most current version of Form W-7 from IRS.gov rather than using outdated versions. Complete all required sections, including personal information and Line 6h where you select your exception category.

Organize your application package with Form W-7 on top, followed by identity documents, then all exception-specific supporting documentation in logical order. Use paper clips to hold documents together rather than staples.

Mail your complete application package to the appropriate IRS address listed in the current Form W-7 instructions. Use certified mail or a trackable delivery service to confirm receipt and have proof of mailing date.

Can I apply for an ITIN without a tax return if I don't fit any exceptions?

No, if you do not qualify for one of the five specific IRS-approved exceptions, you must attach a federal tax return. Attempting to claim an exception you do not qualify for will result in rejection.

Which ITIN exception is most common?

Exception 2 (tax treaty benefits) and Exception 3 (scholarship income) are the most common exceptions used annually. International students represent a large percentage of exception-based applications.

How long does exception-based ITIN processing take?

Exception-based applications process in the same timeframe as regular applications: typically seven to eleven weeks. Claiming an exception does not expedite processing.

Do I still need identity documents if I use an exception?

Yes, all ITIN applicants must submit acceptable identity documents regardless of whether they use an exception. Exceptions eliminate only the tax return requirement.

What if I qualify for multiple exceptions?

Select the single exception that best fits your primary reason for needing the ITIN. You can only check one exception box on Form W-7.

What happens if the IRS rejects my exception claim?

The IRS will mail you a letter explaining why your exception was not accepted. You will need to provide better documentation or reapply with a tax return attached.

Exception-based ITIN applications involve complex qualification criteria and specific documentation requirements that benefit from professional guidance. Tax treaty exceptions under Exception 2 require interpretation of bilateral international agreements and precise treaty article citations.

Real estate transactions under Exception 4 often involve time pressure from closing deadlines and coordination with buyers and attorneys. Professional ITIN assistance ensures you select the correct exception category for your circumstances.

Our tax professionals at Easy Tax Store specialize in exception-based ITIN applications across all five exception categories. We analyze your situation to determine which exception applies and prepare all required supporting documentation.

Schedule a consultation to discuss your specific exception situation and receive a professional analysis.

Conclusion

You can successfully apply for an ITIN without filing a US tax return if you qualify for one of five specific IRS-approved exceptions. The five exceptions cover third-party withholding on passive income, tax treaty benefits with four subcategories, scholarship and fellowship income, FIRPTA withholding on real property sales, and dependents of US taxpayers.

Each exception has precise documentation requirements that must be submitted with Form W-7 to prove your qualification. Exception applications process in the same seven to eleven week timeframe as regular applications.

Most ITIN applicants do not qualify for exceptions and must file federal tax returns with their applications under standard procedures. Carefully review the exception requirements and assess your genuine qualification before claiming any exception.

If you qualify for a legitimate exception, gather all required documentation and begin your application with confidence. If uncertain about exception eligibility, consult with professionals to ensure correct exception selection and complete documentation.